Formerly known as

Life insurers require a lot of information before giving a potential client cover.

They have been one of the pioneering industries in the data and analytics space for more than a century. They use a combination of data to estimate when you might die to calculate the risk of you dying within your policy term to determine the cost of insuring against this.

The more likely they are to have to pay out the more it will cost to insure your life.

One of the biggest predicting factors to when you will die is your age. Other key factors include your gender, and your personal and/or family medical conditions.

Life Insurance companies have a team of people, called Actuaries, who use complex formulas to create ‘life tables'. These tables are used to predict when someone might die based on their age and other specific life factors. These tables are updated when there is more data to analyse. Cheery stuff!

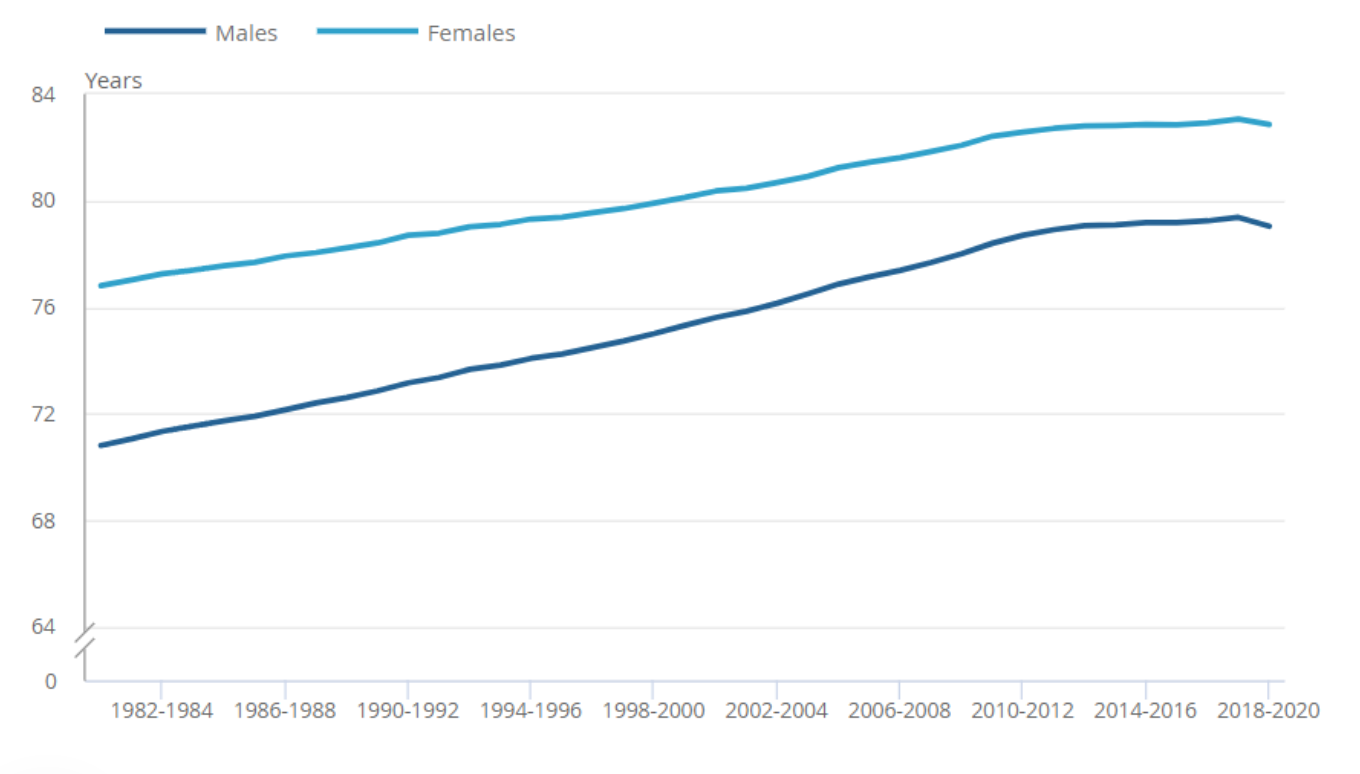

It’s not just life insurers who use life expectancy and life tables to work out when someone might die, it’s also important for governments to understand this. The ONS also produces data on the life expectancy of people in the UK.

Life expectancy in the UK varies by gender.

Life expectancy by gender is as follows:

Male: 79 years

Female: 82.9 years

Life expectancy has been increasing in the UK over the last 40 years, but has slowed in the last decade. Covid has also affected this data as there were more deaths in 2020.

Yes, you can check your own life expectancy according to the ONS by looking at when you were born.

However, the ONS is using averaged data from across the UK.

Whereas Life Insurers use more tailored data from you on your personal medical information and family medical history to predict your age of death.

The higher your life expectancy the lower your monthly premiums are likely to be.

This means that it’s not worth holding your breath when it comes to sorting your Life Insurance. Ticking this not-so-exciting piece of life admin off your list sooner rather than later can save you money in the long run.

Life expectancy is important in calculating the potential return from a Life Insurance policy. According to Investopedia, the return on investment (ROI) for Life Insurance is

Payout - the amount paid into the policy when you die = ROI

If you are covered for £150,000 and pay in £48,000 then your ROI is £102,000.

Using your life expectancy you can start to calculate this for differing levels of cover and term lengths you may be considering.

Of course, there are other factors you may want to take into account when deciding on your policy. You may want to consider:

All of these things are used by Life Insurance calculators to decide how much cover you may need.

Latest data from the Association of British Insurers (ABI) show that around £17 million is paid out every day. That’s just over £6 billion a year.

The average UK payout on term Life Insurance was £79,304 - with 98% of all claims paid.

Of the claims there were not paid, the most common reason was non-disclosure; so remember it’s key to be honest when applying for a policy.